February 2, 2021

New Word on Preferred Stock Treatment

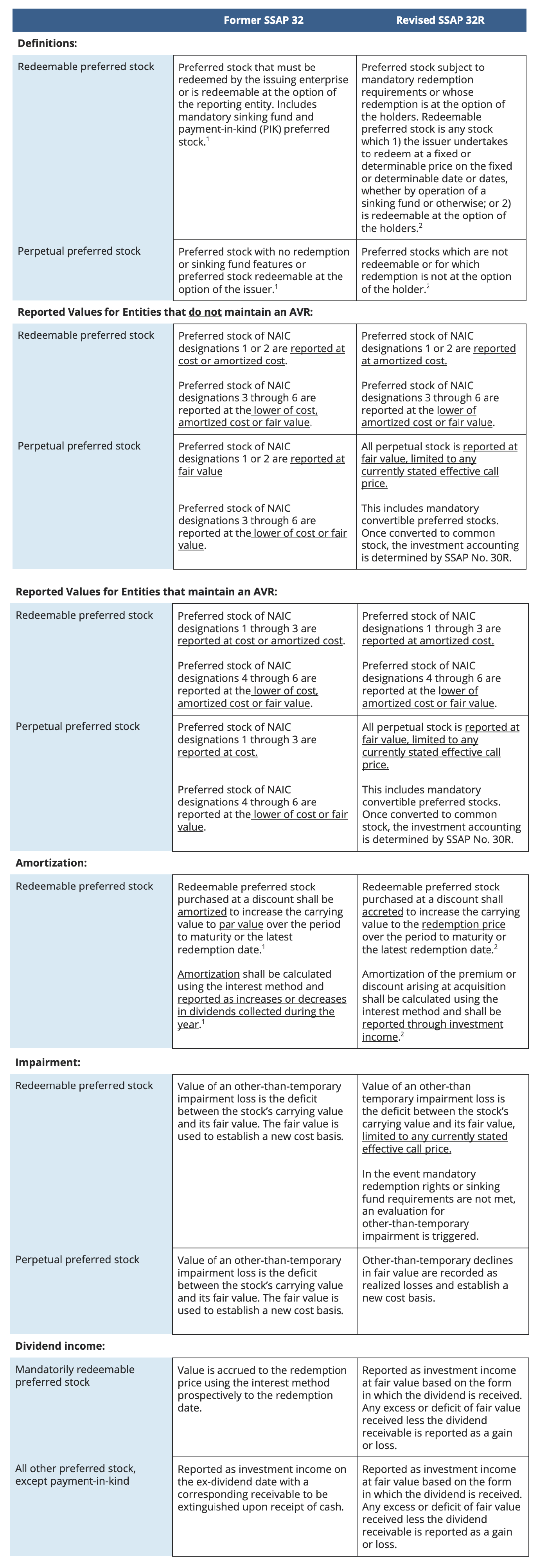

One of the anticipated changes stemming from the NAIC’s Investment Classification Project took effect for statutory filers on January 1, 2021, with early adoption permitted for 2020 reporting periods. The accounting guidance for preferred stock was revised to more closely resemble U.S. GAAP. Some of the primary changes implemented with SSAP No. 32R – Preferred Stock (NAIC Ref #2019-04) are:

- Updates the definitions of redeemable, perpetual, and restricted preferred stock to make them more harmonious with U.S. GAAP terminology and concepts

- Changes reported values of redeemable and perpetual preferred stock

- Incorporates specific guidance for valuing mandatorily convertible preferred stock

- Clarifies other-than-temporary impairment assessment for redeemable preferred stock

- Clarifies accounting treatment for dividend income received from preferred stocks

Consistent with the former statutory guidance, the classification of preferred stock as redeemable or perpetual, and if the reporting entity maintains an asset valuation reserve (AVR), determines the applicable accounting treatment of preferred stocks. To ensure compliance, companies with preferred stock holdings must first review their portfolio to assess if classification of any holdings are modified under the new definitions. Then, companies will need to verify preferred stock balances and investment income are reported in accordance with the revised guidance, both for preferred stocks which did not change classification and those that did.

A summary of the guidance before and after adoption of the preferred stock changes follows:

SSAP No. 32R applies to life, health, and property and casualty insurers. Issue Paper No. 164, published by the NAIC, discusses the rationale for these changes in greater detail.

1SSAP No. 32 – Preferred Stock

2SSAP No. 32R – Preferred Stock

Have any questions regarding these changes? Contact the Johnson Lambert team.